If you’re dreaming of getting on the property ladder but not quite ready to buy your forever home, you might be wondering:

Can I buy an investment property first — even before I buy a home to live in?

The answer is: Yes, you can. And for many people, (especially people in the south), it’s a smart move.

Let’s dive into how it works, the pros and cons, and what to consider financially.

💸 You Can Invest First — But Here’s How It Works

Buying a buy-to-let property before your own residential home is entirely legal — and in many ways, more financially strategic.

However, there are key differences:

🏠 Residential Mortgage (for your own home):

- Usually requires a lower deposit (10% or even less with a Help to Buy or similar scheme)

- Often has lower interest rates

- You must live in the property

🏘️ Buy-to-Let Mortgage:

- Usually requires a larger deposit (typically 25% of the property value)

- Higher interest rates (as it’s considered higher risk)

- Based on rental income, not your salary alone

- You can’t live in the property yourself

So yes — you can legally and financially own a rental property first, but the type of mortgage, deposit, and criteria are very different.

✅ The Pros of Buying an Investment Property First

- Start Building Wealth Sooner

While you’re saving for your dream home, your investment property can be earning rental income and increasing in value over time. - Affordability

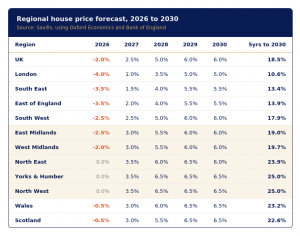

Many people based in the South have chunks of cash saved, but cannot get residential lending for their own home as you can only get residential lending up to 4.5-5X your annual salary and property there is no longer at an affordable price - Let Your Investment Work for You

If your buy-to-let increases in value, you can remortgage it in a few years to release equity — potentially helping you fund your own home later. - You’re Not Tied to One Location

If your job or lifestyle is flexible, you don’t have to buy where you live. You can invest in a high-yield area (e.g., the Midlands or North) and rent where you want to live — often called “rentvesting.” - Tax-Efficient Long-Term Strategy

If structured properly (e.g. through a limited company), investing first can set up a more tax-efficient foundation for future portfolio growth.

⚠️ The Cons and Considerations

- Higher Deposit Needed

Buy-to-let typically requires 25% deposit, so it’s not always easier than buying a first home. However, targeting more affordable locations in the North can still mean it’s affordable. - You May Not Qualify for First-Time Buyer Schemes

If you buy an investment property first, you lose access to schemes like Help to Buy or shared ownership. - You’ll Still Need Somewhere to Live

If you’re renting your home while owning an investment property, make sure it fits your lifestyle and doesn’t feel like a sacrifice.

🔢 Let’s Talk Finances (All figures below are used as examples)

Here’s a rough breakdown of costs for a £160,000 buy-to-let property:

- Deposit: £40,000 (25%)

- Stamp Duty: £5,500 (incl. 3% surcharge)

- Legal & Mortgage Fees: ~£2,000

- Furnishing / Letting fees: £1,500–£3,000

If the property rents for £900/month, and your mortgage and costs are £600/month, that’s a £300/month income — or £3,600 per year.

💼 Is It Right for You?

Buying an investment property before your first home is not for everyone, but it’s an increasingly popular strategy for:

- People priced out of their local area

- Ambitious savers who want to build wealth fast

- Those who see property as a business, not just a roof over their head

If done with the right guidance, it could accelerate your path to financial independence — and even make it easier to afford your first home later on.

👋 Final Word: Use Strategy, Not Emotion

Your “first step on the ladder” doesn’t have to be the house you live in. With property prices rising and rental demand booming, it can make sense to let your money work harder somewhere else first.

Just make sure you’re not doing it alone — working with a property investment expert helps you find the best areas, strongest yields, and growth potential so you can make confident, informed decisions. If you’re looking to discuss whether this might be right for your situation and would like a free consultation then please get in touch here: https://fraterpropertypartners.com/contact/