Headlines love a crash narrative. It gets clicks, it spreads fast, and it plays perfectly into the natural fear most investors have about buying at the “wrong” time. The problem is, the same headlines have been screaming about an imminent property crash for years, and the people who listened too closely often ended up sat on the sidelines while rents were collected and prices quietly moved on in the background.

At Frater Property Partners, we help investors build passive wealth through property. This means we need to be confident on what is actually happening in the property market and what the data really suggests.

So let’s strip this back to one simple question: is there real data behind the “2026 crash” narrative, or is it mostly noise?

Why people believe a crash is coming

There are two main reasons this idea keeps resurfacing. The first is the memory of the interest-rate shock, and the uncertainty it created across 2024 and 2025. Higher borrowing costs changed affordability, slowed activity, and made people assume the next step must be a sharper correction.

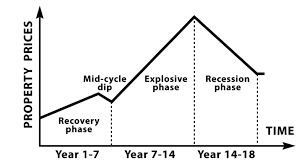

The second is the “18-year property cycle” theory. The logic goes like this: 18 years after the last major crash in 2008 brings us to 2026, and therefore the market should crash again. It’s a compelling story because it feels neat and predictable. The issue is that property isn’t governed by tidy calendar patterns; it’s governed by supply, demand, credit conditions, and confidence.

Even mainstream media has been revisiting this cycle theory recently, largely because it makes for a punchy narrative.

What the 18-year cycle gets wrong in today’s UK market

The classic boom-bust framework assumes that markets crash because of oversupply and speculative excess. In the current UK housing market, the more persistent issue is the opposite: chronic undersupply. When supply is structurally tight, prices don’t behave like a textbook overbuilt market. They behave like a rationed asset where affordability and access determine where growth happens, not whether the whole market collapses at once.

You can see this in official housing supply data and ongoing reporting: delivery has remained below what’s needed, and completions have been volatile. That matters because shortages don’t guarantee prices rise everywhere, but they do make an across-the-board crash far less likely unless something breaks on the demand side, such as a major credit crunch or a deep recession.

The other modern factor is demographic drag on supply. People are living longer and staying in homes for decades, which reduces churn and keeps family-sized housing in short supply. That’s not a “headline” factor, but it’s a real-world constraint on available stock, especially in the most desirable owner-occupier pockets.

In plain English, this is why the national average is becoming less useful. Some areas can cool or fall while others stay resilient or grow, because the drivers are local.

What the data is actually saying right now

If you want a more grounded view of 2026, look at what the professional surveyors and major research houses are reporting rather than what the loudest headlines are shouting.

RICS survey data published on February 12, 2026 pointed to early signs of recovery in sentiment and expectations for sales over the coming year, while still acknowledging activity remains subdued and recovery may be gradual. That doesn’t read like a market about to fall off a cliff. It reads like a market stabilising after a long affordability squeeze.

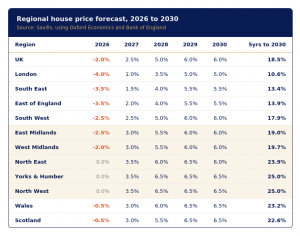

Savills’ own UK market commentary and forecasts have also leaned toward stability and gradual improvement rather than a crash scenario. Their July 2025 revised mainstream forecast projected modest growth near term and stronger cumulative growth over five years, reflecting an expectation of improving conditions as the rate environment normalises. Their January 2026 update also highlighted that growth has been stronger in the North West than in London on the latest annual readings, reinforcing the point that regional divergence is doing the heavy lifting.

Even in prime markets, Savills’ commentary for 2026 points toward greater stability and a gradual recovery profile rather than a sharp downturn.

So, is a crash impossible? No. Property is cyclical and it’s always exposed to macro shocks. But the burden of proof sits with the crash narrativeand right now the data looks more like “slow recovery + regional divergence” than “systemic collapse.”,

The scenario that could still hurt prices

If you want to stress-test your thinking, the real “crash catalysts” tend to be less about calendar cycles and more about sudden breaks in credit and employment. A sharp tightening of mortgage availability, a meaningful unemployment spike, or a major recession can force distressed sales and change price dynamics quickly. That’s the black swan side of property.

But in a world where supply remains constrained and rental demand remains strong, widespread forced selling becomes harder to manufacture without a deeper macro event.

What we expect 2026 to look like for investors

The most realistic outlook is not “boom” or “bust.” It’s consolidation. Rates stabilise, affordability gradually improves for buyers and investors, and the market increasingly rewards people who buy in the right places, at the right price, with the right strategy.

That “right place” point is key. London and parts of the South East are still wrestling with affordability ceilings, while many regions with stronger affordability and job growth dynamics can continue to show resilience. Research and market updates repeatedly point to this regional pattern.

This is also why serious investors stop obsessing over the next 12 months and start planning like portfolio builders. Property works best when it’s held long enough for refinancing, rental growth, and compounding to do their job. Even if you bought at a market peak historically, the investors who held through the cycle and managed the asset well were rarely the ones who lost in the long run; the panic sellers were.

The investor move: stop trying to time the market and start timing your strategy

If your goal is to build a portfolio, your advantage is not predicting a crash. Your advantage is buying assets that can handle a range of outcomes. That means you underwrite deals for resilience rather than optimism. You want stock that still works if rent growth is slower, if rates take longer to ease, if you have a void, or if maintenance costs rise. You also want locations where demand isn’t dependent on a single employer, a single tenant type, or a single hype story.

That’s exactly how we approach opportunities at Frater. We don’t ask clients to get involved in the negotiation or the back-and-forth. We do that on their behalf so we can secure strong terms and keep the process clean, fast, and professional, especially when we’re packaging demand across multiple investors.

If you want to build your portfolio, and not sure where to start then get in touch today for a free chat with one of the team: https://fraterpropertypartners.com/work-with-us/