BRRR, which stands for Buy, Refurbish, Refinance, Rent, is one of the most talked-about property investment strategies in the UK right now. It’s also one of the most misunderstood. Done well, it allows investors to recycle the same pot of capital across multiple acquisitions, building a portfolio faster than a standard buy-to-let approach would allow. Done carelessly, it ties up capital, produces down valuations, and leaves investors stuck.

So does it actually work in 2026? The honest answer is yes, but the margin for error has narrowed. The strategy now rewards preparation rather than optimism, and discounted purchases alone no longer compensate for weak exit planning. This guide explains exactly how BRRR works, what the numbers look like in practice, and where the strategy succeeds and fails in the current market.

How BRRR Works: The Core Cycle

The cycle has four stages, each of which needs to work for the overall model to function.

Buy below market value. The discount at acquisition is what creates the equity buffer that makes the refinance viable. If you buy at market value with no discount, the refinance valuation rarely returns enough capital to make the model work. The BMV purchase is not optional. It is the foundation the entire strategy is built on.

Refurbish to a standard that forces the valuation higher. The goal is not the most expensive finish. It’s the most value-efficient finish relative to what the local market will support. A £30,000 refurbishment that adds £45,000 of value works. A £50,000 refurbishment that adds £40,000 of value doesn’t, regardless of how good it looks.

Refinance onto a standard buy-to-let mortgage at 75% LTV based on the new higher valuation rather than the original purchase price. This is where capital is recycled back out of the deal and made available for the next acquisition.

Rent the property at a level that covers the mortgage, running costs, and generates positive monthly cashflow. The rent also needs to satisfy the lender’s stress test requirements before the refinance can be approved.

A Worked Example: What the Numbers Actually Look Like

Here’s a realistic example using a terraced house in a strong northern or Midlands market in 2026.

Purchase price at 15 to 20% below market value on a £162,500 market value property: £130,000. Buying costs including stamp duty, solicitor fees, and survey: approximately £13,500. Refurbishment budget including 15% contingency: £34,500. Total capital invested: £178,000.

Post-refurbishment valuation at £1.50 added value per £1.00 spent: £207,500. Refinance at 75% LTV: £155,625. Refinance costs: £3,000. Capital recycled after refinance: £152,625. Capital left in the deal: approximately £28,375. Retained equity in the asset: approximately £51,875. Monthly rent at 6% gross yield on post-refurbishment valuation: £1,037.

The capital left in the deal, approximately £28,375 in this example, determines how quickly you can move to the next project. Buying at a steeper discount, executing a more value-efficient refurbishment, or achieving a stronger post-refurbishment valuation all reduce this figure and accelerate the cycle.

The Stress Test: What Lenders Actually Require

Before a lender will offer a buy-to-let mortgage at the refinance stage, the rental income needs to pass an affordability stress test. Most UK buy-to-let lenders in 2026 stress test at 5.5% with an Interest Coverage Ratio of 125% for limited company purchases and 145% for personal name purchases.

In plain terms, the monthly rent must cover at least 125% of what the monthly mortgage payment would be if the interest rate were 5.5%, regardless of the actual rate on the product you’re taking.

On a £155,625 loan stressed at 5.5%, the monthly interest is approximately £713. At 125% ICR, the minimum monthly rent required to pass is £891. The projected rent of £1,037 in the example above passes comfortably. But on a larger loan in a market where yield is harder to achieve, this stress test becomes a real constraint that needs to be modelled before exchange, not after.

For investors purchasing through an SPV, the 125% ICR applies. For personal name purchases, lenders typically require 145%, which materially increases the minimum rent needed. This is one of the primary reasons the SPV structure is standard for serious portfolio investors.

Is BRRR Right for You? The Honest Answer

This is the part most property content skips over, and it matters more than anything else on this page.

BRRR is a more complex, more time-intensive, and higher-risk strategy than a standard buy-to-let. A standard buy-to-let involves buying a well-located property, placing a tenant, and holding for the long term. The main decisions happen at acquisition. After that, a good letting agent handles the day-to-day and the asset largely looks after itself.

BRRR doesn’t work like that. Every stage introduces a new category of risk. The purchase needs to be at a genuine discount. The refurbishment needs to be scoped accurately, managed tightly, and delivered on time and on budget. The post-refurbishment valuation needs to be supported by comparable evidence. The refinance needs to pass the lender’s stress test. Any one of these stages going wrong affects every stage that follows.

For investors with the time, the experience, and the trades relationships to manage a refurbishment project themselves, BRRR can be executed effectively. But for time-poor professionals, attempting a BRRR project without experienced project management in place is one of the most common and costly mistakes we see in the market.

The issues that arise most frequently are predictable: refurbishment budgets that run significantly over because the scope wasn’t properly defined at the outset, timelines that extend by months because trades weren’t managed proactively, and post-refurbishment valuations that come in below expectation because the finish didn’t match what the local market required. Each of these individually is painful. All three on the same project, which happens more often than most people admit, can turn a viable deal into a significant loss.

None of this means BRRR is inaccessible to time-poor professionals. It means that without the time or experience to manage delivery personally, a trusted delivery partner with a proven track record in the target market is a prerequisite, not an optional extra. The right partner scopes the refurbishment correctly before exchange, verifies post-refurbishment valuation assumptions against real comparable evidence, and ensures the project is delivered to the standard and within the timeline the financial model depends on.

Without that, BRRR carries considerably more risk than the headline numbers suggest. With it, the strategy is one of the most effective ways to build equity quickly in UK residential property.

Where BRRR Works Best in 2026

The strategy performs most reliably where three things are simultaneously true: there is a credible pipeline of below-market-value stock, the refurbishment uplift is supported by local comparable evidence, and the rental demand is strong enough to achieve the yield needed to pass the stress test.

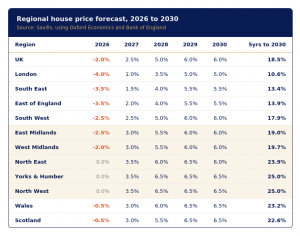

In 2026, the markets that consistently meet all three criteria are concentrated in the North and Midlands. Areas like outer Nottingham, Leicester, Wolverhampton, Wakefield, Huddersfield, Bolton, and Preston offer achievable entry prices, realistic post-refurbishment uplifts, and professional tenant demand that makes the model work in practice rather than just on paper.

Markets to be cautious about are those where the ceiling price is too low to support the post-refurbishment valuation the model needs, and those where the rental market is too thin to achieve the yield required to pass the stress test. Both need to be verified at street level before exchange.

The Four Most Common Reasons BRRR Fails

Buying at or near market value without a meaningful discount. The BMV purchase is the equity buffer that makes the refinance viable. Without it, the model depends on the refurbishment doing all the heavy lifting, which it rarely does to the degree needed.

Refurbishment cost overruns. A budget that runs 20% over doesn’t just reduce the profit on that deal. It reduces capital available for the next acquisition and can push total costs above what the refinance will return.

Down valuations at the refinance stage. If the surveyor values the property below expectation, the capital recycled is reduced and more money stays locked in the deal. The mitigation is to verify comparable sold evidence before exchange, not after.

Failing the lender stress test. If the rental income doesn’t adequately cover the mortgage at the stressed interest rate, the refinance doesn’t proceed. This needs to be modelled against actual rental comparables in the target area before committing to the purchase.

BRRR Versus Standard Buy-to-Let

BRRR generates equity faster than a standard buy-to-let because it creates value at acquisition and through refurbishment rather than waiting purely for market growth. But it requires more active involvement, more capital management, and a stronger team around it to execute reliably.

A standard buy-to-let is a simpler model with fewer moving parts and lower execution risk. The tradeoff is that equity builds more slowly and portfolio growth is constrained by the pace at which the market delivers appreciation.

For time-poor professionals, the right answer often depends on timeline and access to the right delivery partner. BRRR accelerates the equity accumulation phase significantly. Standard buy-to-let provides steadier, lower-maintenance compounding over time. Many serious investors use both in combination, running BRRR projects in the early years to build equity quickly and transitioning toward standard buy-to-let as the income focus becomes more important than the growth focus.

The Bottom Line

BRRR works in the UK in 2026, but it’s not right for everyone. It rewards investors who treat it as a structured process rather than a shortcut. The BMV purchase, the honest refurbishment budget, the pre-exchange comparable check, the stress test verification, and the right delivery team around the project are not optional. They are what separates a deal that performs from one that locks up capital for longer than planned.

The investors who execute BRRR well in the current market are not the ones taking the most risk. They are the ones taking the most care.

Thinking about whether BRRR is the right strategy for your situation? Book a free planning session with the Frater Property Partners team at fraterpropertypartners.com/work-with-us/