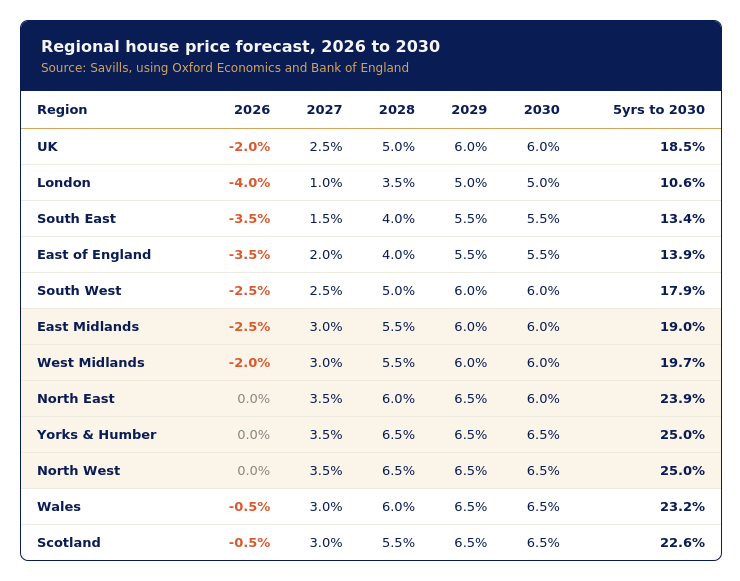

Savills has revised its 2026 UK house price forecast from 2% growth to a 2% decline. The shift reflects mounting pressure on household finances amid higher borrowing costs and persistent inflation.

Headlines like this tend to generate more anxiety than insight. At Frater Property Partners, we help time-poor professionals build long-term residential portfolios across the Midlands, Yorkshire, and the North West, and questions like this come up constantly. So here’s what’s actually driving the revision, and why the regional picture tells a very different story to the national one.

What Changed

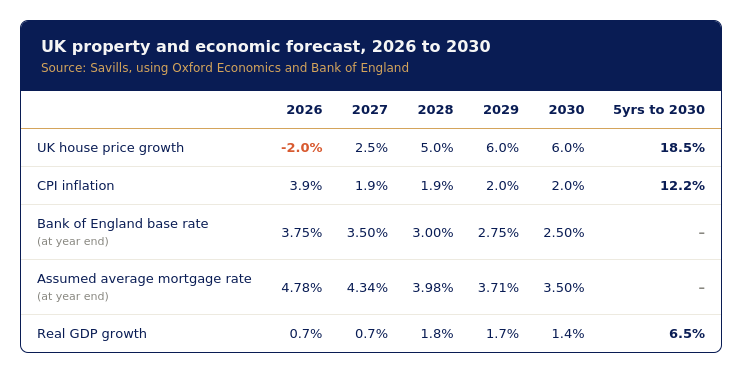

House prices rose by 2.0% in the first four months of 2026. Both price growth and activity were relatively robust. Then mortgage rates moved. Lucian Cook, Savills’ head of residential research, put it simply: “The rise in mortgage rates since late February has downgraded the short-term outlook.”

Inflation is now forecast to hit 3.9% by year end, with the base rate held at current levels until late 2027. Buyer enquiries have already softened in response. The RICS survey shows new buyer enquiries running at a net balance of negative 37 across March and April, against an average of negative 24 in the prior six months.

There’s a second pressure stacking on top of this. Landlords are selling up in the face of greater regulation, adding to stock levels just as demand softens, with the effect most pronounced in London and the South East. That’s the regulatory headwind we’ve flagged before. The Renters’ Rights Act came fully into force on 1 May 2026, and the bulk of its reforms, including the abolition of Section 21 evictions and the shift to periodic tenancies, are now live. The compliance burden that’s followed is accelerating exits among less professional landlords, and that supply is landing in a softer market.

Why This Isn’t 2022

Affordability has improved compared with 2022, and stricter lending rules combined with widespread fixed-rate mortgages have reduced the likelihood of forced sales. This is a temporary affordability squeeze, not a structural correction.

The Five-Year Picture Is Barely Moving

Savills still expects 18.5% growth by 2030, down from 22.2%. That’s a revision to the path, not the destination. Growth resumes at 2.5% in 2027, 5% in 2028, and 6% annually in 2029 and 2030. Mortgage rates are expected to fall from 4.78% to 3.50% over the same period.

A market being squeezed by borrowing costs today is, by Savills’ own modelling, expected to see those costs ease meaningfully within four years.

Where It Gets Interesting: The Regional Split

This is the number that actually matters if you’re investing outside London.

Yorkshire and Humber and the North West are projected to see 25% growth by 2030. London is forecast at 10.6%. More than double. By 2030, North West values are expected to sit just 15% below the UK average, narrowing from nearly 30% a decade earlier.

This isn’t new. Dan Hill, Savills’ research analyst, explains the mechanism: “Since 2016, we’ve been in the second half of the cycle, where the more affordable regions in the North and Scotland outperform the UK average, and capacity for growth in London and the South is more limited.” That pattern is expected to persist for the next five years.

For anyone thinking about yield compression and where real capital appreciation sits over a five to ten year hold, this is the data point that matters more than the national headline. It’s also the reason our acquisition focus has consistently sat in these markets rather than chasing national headlines.

What It Means for BRRR and Buy-to-Let

A meaningful amount of stock is moving from smaller, often longer-standing landlords toward larger, more professional operators, a trend that’s expected to continue now the Renters’ Rights Act is in force. Many of these are landlords who’ve held properties for decades, often acquired well before today’s compliance standards existed, and who are choosing this point to step back rather than retrofit a portfolio that was never built with the current regulatory landscape in mind.

That’s not a reason for newer or smaller investors to be nervous. It’s the opposite. It’s creating genuine opportunity for anyone approaching property with the right structure and the right standard of due diligence from the outset. Properties acquired and run properly from day one are far better positioned to navigate this environment than those that have drifted for years without it. The lesson isn’t that small landlords are in trouble. It’s that the bar for doing this well has risen, and the investors who meet that bar are the ones picking up genuinely well-priced stock from people exiting on their own terms.

The risk worth flagging: a more protracted conflict in the Middle East could push inflation and rates higher again, triggering more short-term pressure followed by a sharper recovery. This is exactly why we stress-test every acquisition against a higher rate environment before committing, rather than relying on the most optimistic scenario.

Why This Doesn’t Change Our Approach

We work in the Midlands, Yorkshire, and the North West because the fundamentals here have supported this kind of outperformance long before this forecast existed. Our deals are never built on national price momentum. They’re built on rental demand, employment diversity, and acquisition pricing that holds up regardless of which way the wider market moves.

A 2% national dip against 25% projected growth in our core markets doesn’t change that. It confirms it.

The Bottom Line

2026 is softer nationally, for an identifiable reason that isn’t structural. The five-year picture is barely changed. And the regional gap between the South and the North, Midlands, Scotland, and Wales isn’t a blip. It’s a cycle that’s been running since 2016 and isn’t expected to turn for another five years.

Headlines about national price falls tell you almost nothing useful. The regional data tells you everything.

Quick Answers

Is now a good time to invest in property in the North of England? Yes, on the data available. Savills projects 25% growth in Yorkshire and the North West by 2030, more than double London’s forecast of 10.6%, driven by stronger affordability and a housing market cycle that has favoured these regions since 2016.

Why is Savills predicting a house price fall in 2026? Rising mortgage rates following instability in the Middle East have pushed inflation higher and delayed expected interest rate cuts, reducing buyer affordability in the near term. Savills describes this as a temporary squeeze rather than a structural downturn.

Will the Renters’ Rights Act affect property investment opportunities? It’s already having an effect. Since coming into force on 1 May 2026, it has accelerated the exit of longer-standing, less compliance-focused landlords, creating opportunities for professional investors buying and managing assets to a higher standard.

Want to talk through what this means for your portfolio? Book a free planning session with the Frater Property Partners team at fraterpropertypartners.com/work-with-us/